S&P 500: A Temporary Pullback, But the Long-Term Uptrend Remains Intact

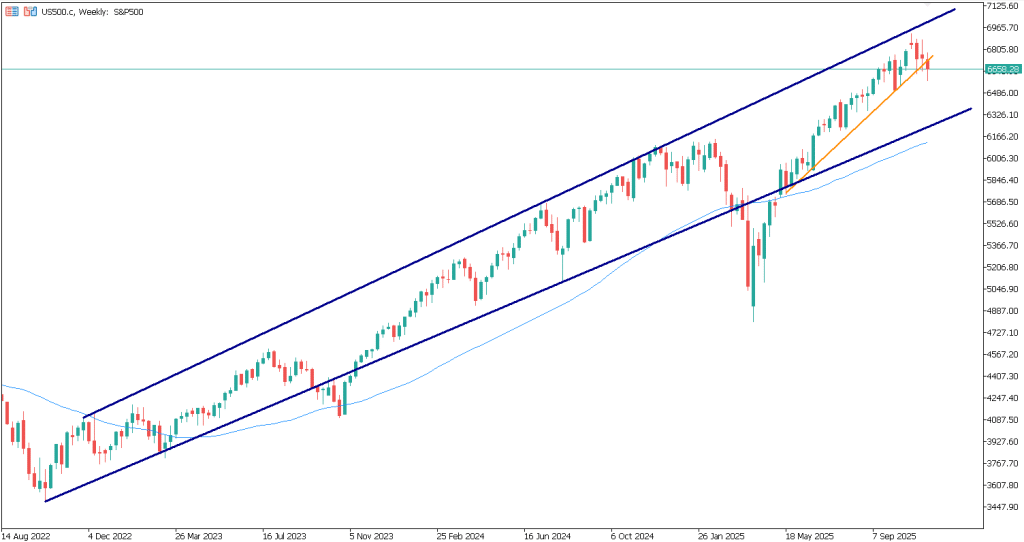

Despite the recent pullback from all-time highs and a sharp rise in negative narratives, the S&P 500 continues to hold its long-term bullish structure. While a shorter-term trendline – formed after Trump’s tariff shock – has now been broken, a much broader and more meaningful trendline that has been active since 2023 remains intact. The index is currently testing its lower boundary, suggesting that the latest correction is not, at least for now, a structural trend reversal.

US500 chart, November 18, 2025. Source: TenTrade.com

What Triggered the Pullback?

The correction began immediately after the latest FOMC meeting, where the Fed unexpectedly downplayed the likelihood of a rate cut at the upcoming meeting.

Markets had positioned heavily in anticipation of that cut, and the repricing that followed triggered forced adjustments across equities – particularly in interest-rate-sensitive and long-duration sectors.

At the same time, turbulence in the repo markets, the core liquidity channels of the U.S. financial system, tightened liquidity and amplified the downside. These stresses, combined with renewed fears surrounding a supposed “AI bubble,” created the perfect environment for a short-term risk-off move.

Synthesis: Repo Stress as the True Catalyst Behind the Market Reversal

The primary driver of the recent reversal in equities is stress in the private repo markets (short-term borrowing using securities as collateral) – not simply fear of an AI bubble or the Fed’s tone shift.

QT and the recent rise in the Treasury General Account have drained liquidity, pushing private repo rates higher as institutions aggressively bid for cash. Gitler argues that this environment reveals that bank reserves are far less abundant than many believed, pushing leveraged funds toward de-leveraging. With financing becoming more expensive and less accessible, leveraged players are being forced to unwind positions – directly weakening equity momentum.

In this view, liquidity mechanics- not sentiment headlines – have been the dominant force behind the pullback.

Understanding the Liquidity Dynamics

Part of the repo stress stems from the TGA rebuild (government replenishing its main Treasury cash account), which has withdrawn liquidity from the banking system just as QT continues to shrink reserves.

On top of that, institutions that cannot earn IORB (interest the Fed pays banks on reserves – such as certain money market funds and hedge funds) have been bidding aggressively for repo liquidity, pushing private rates higher and crowding others out.

This dynamic matters because leveraged funds rely heavily on repo financing to fund positions in equities, futures, and basis trades.

As repo rates rise and availability shrinks, those funds face a clear message: financing is no longer cheap or guaranteed.

The result is forced position-cutting, reduced leverage, and weaker risk momentum – exactly what we’ve seen in the markets over recent sessions.

A Mild Correction Given the Level of Fear

Despite these clear liquidity pressures, the correction in the S&P 500 has been just around 5%, and slightly more in the Nasdaq.

When markets are dominated by fears of liquidity crises, AI bubbles, uncertain Fed policy and extreme sentiment readings, we might expect a far deeper sell-off.

But that’s not what happened.

The relatively shallow correction suggests robust underlying demand, strong institutional support at key technical levels, and an uptrend that remains decisively intact on a multi-year basis.

What Could Ease the Liquidity Stress?

We highlight several potential catalysts that could relieve pressure in the repo markets and shift the tone in equities:

- The end of the government shutdown, which would normalise the TGA and stop draining liquidity.

- A potential slowdown or adjustment to QT, which would allow reserves to stabilise or begin rebuilding.

- A reduction in private repo demand as financing conditions normalise.

The message is clear: Improving liquidity could quickly restore risk appetite, while persistent stress could cap upside and create the risk of another leg lower.

Risks Persist, But the Long-Term Trend Holds

Even with repo stress, FOMC uncertainty, and volatility in the AI sector, the multi-year trendline from 2023 remains unbroken.

This is the key technical level that defines whether we are in a cyclical correction or a structural trend reversal.

For now, the data supports the former, not the latter.

Conclusion: A Liquidity-Driven Pullback, Not a Trend Reversal

The recent weakness in equities appears to stem primarily from temporary liquidity stress in repo markets, amplified by a hawkish-leaning Fed tone and sentiment-driven fears around AI.

Yet despite all these pressures, the correction has been shallow, and the S&P 500 continues to hold its long-term uptrend.

Bull markets do not end because investors are afraid – they end when liquidity dries up and trends exhaust.

So far, we are seeing stress but not exhaustion.

There may be fear in the markets and apocalyptic narratives but the correction is “mild” and this may signal a bottom. The long-term bullish structure remains intact, pending clearer signals from repo markets, TGA flows, and QT dynamics.